How to save £1bn

Every little helps

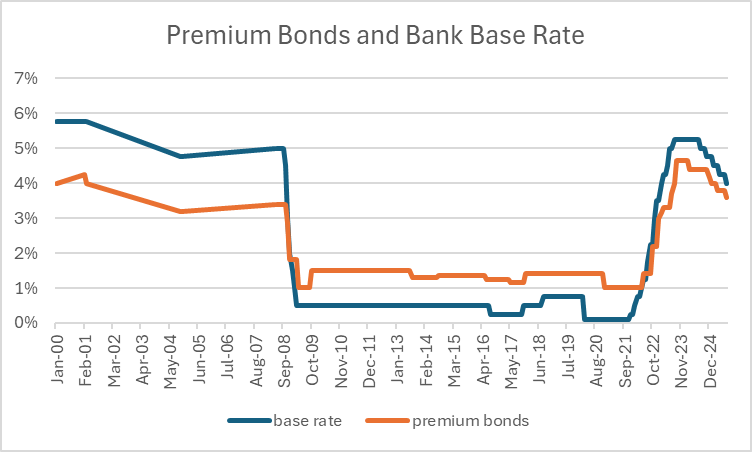

The Chancellor is in a fiscal pickle. In her Budget last year she said that she would not come back for another tranche of tax rises. Three things will force her to do exactly that. First, the government’s failure to kick-start growth. Sure, tariffs and the like don’t help, but putting up employers’ national insurance was bound to hit employment in the …